NZSA Disclaimer

Since KiwiSaver’s launch in 2007, the national conversation has been focused almost entirely on savings accumulation.

Join. Contribute. Stay the course.

But for a growing number of New Zealanders, that chapter is closing. The question is no longer simply “Are we saving enough?” It is increasingly “How do we spend well?”

This is a very different conversation – borne of the emerging luxury of the savings-driven lifestyle created by a growing KiwiSaver.

The question sits at the heart of de-cumulation — the process of converting accumulated savings into sustainable retirement income. In a New Zealand context, the benefit provided by accumulated investments (such as KiwiSaver) sits alongside that provided by NZ Superannuation.

All of that should be aimed at ensuring that we have the financial flexibility we want to support our retirement goals.

Some Background

In my November 2025 article, I discussed the potential benefits of considering the next evolution of KiwiSaver and outlined the key issues that could become relevant for KiwiSaver investors as we close in on the general election later in 2026. In the context of future challenges to National Superannuation affordability and the role of individual investor accountability, our support for the ongoing encouragement of KiwiSaver to support key retirement savings goals for New Zealanders remains steadfast.

I also highlighted that NZ Superannuation has a value to us all – even newborns. That affects how we think about the pace of transition from a reliance on universal superannuation to a greater role for accumulated investment.

Spending well: an independent retirement

For most of our working lives, the investment goal is clear: maximise long-term growth. A twenty-something investor can tolerate volatility because time is on their side, flexibility that is less well-tolerated by most investors in their 60’s.

For an investor nearing retirement, the objective changes. Instead of maximising growth over 40 years, the focus shifts to generating reliable income, managing market volatility, protecting against inflation and ensuring capital lasts for potentially two decades or more.

That’s the financial objective at any rate.

On the personal front, objectives will differ widely. Ultimately, the financial freedom to create choice during your retirement is what matters. True wealth is (arguably) based around the ability to exercise your choices at any time.

There are numerous authors and commentators advocating for how we can consider spending well to support an independent retirement lifestyle.

It’s not just about “affording” retirement, its about spending to support personal objectives. That might mean ticking off those items on your bucket list, while you still have the physical means and health to do that.

From a ‘legacy’ perspective, chances are that your nearest and dearest are likely to benefit from receiving your legacy earlier rather than later. That might mean the ability to enable early inheritance for your children at a point in time when they really need it (eg, buying a house) or creating space for a large donation to your favourite charity.

Retirement itself is becoming a more fluid concept. While NZ Superannuation predicates “retirement” at age 65, many work well beyond that age, simply because they love what they do. Others consider themselves ‘retired’ at age 50.

From an investment perspective, this is not just about a change in asset allocation. Accumulation is about building wealth. De-cumulation is about deploying it.

Enabling a great retirement

It is worth noting that for many, this discussion remains aspirational if discussing the value of investments alone.

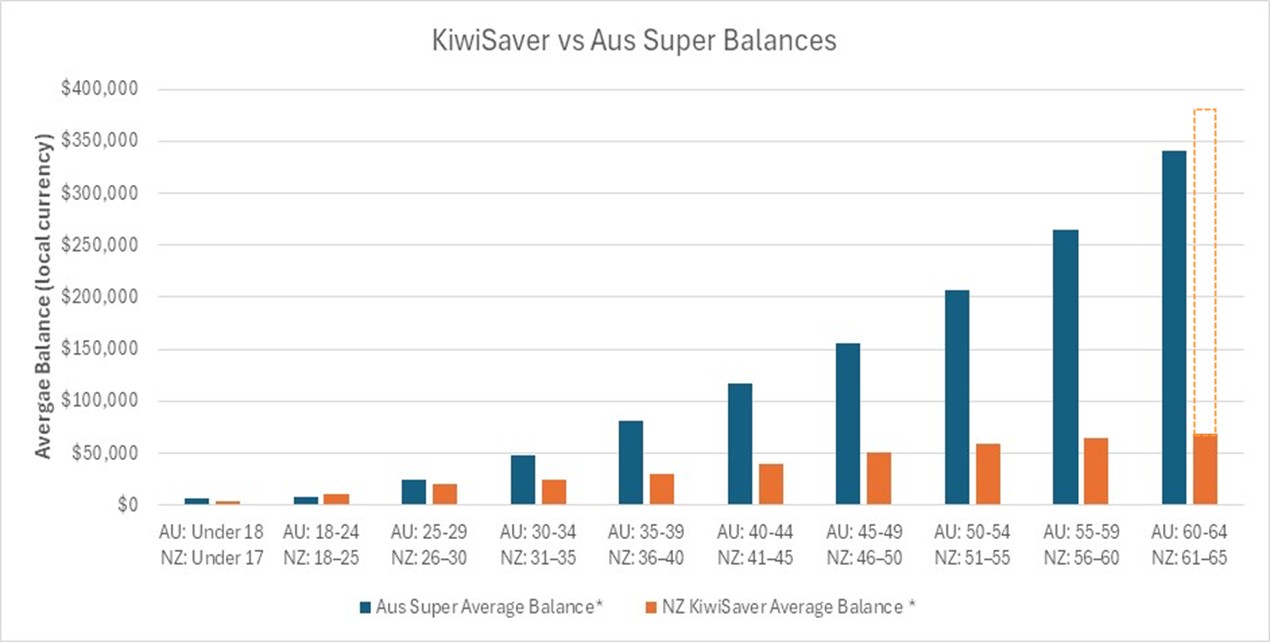

As of December 2024, average KiwiSaver balances for members aged 61–65 sit at approximately $69,000. On the face of it, this looks very different to Australia’s average balance for the same age bracket of AU$340,000.

However, when the ‘capitalised value’ of NZ’s universal superannuation entitlement is included, this results in a much more equal comparison between the two countries. The capitalised value is simply the lump-sum equivalent value of the lifetime stream of annual benefits provided by NZ Superannuation.

Australia does not offer a universal superannuation entitlement, with a much greater reliance on personal investment. Government-funded superannuation is available, but is subject to means testing.

So, the core question of “How do we spend well?” remains. A key takeaway from the data is that most New Zealanders are still very reliant on NZ Superannuation. Any shift towards a more investment-focused approach is generational in nature. This is supported by a September 2025 study[1] undertaken by the Retirement Income Interest Group (RIIG) from the NZ Society of Actuaries: “Any reduction in NZ Super will therefore be challenging for nearly all the population, even if KiwiSaver contribution rates increase to a matched 5% of salary.”

In Australia, given that retirement income is heavily based on investment, the conversation is fast moving towards de-cumulation. As KiwiSaver balances continue to increase, we are likely to see the same trend here.

De-cumulation is a natural consequence of a more investment-focused, “save as you go” retirement planning approach. Converting savings into sustainable retirement income is emerging as the next personal finance challenge for those who have benefitted from a focus on savings and investment over the last 20 years.

How much is enough?

Retirement is no longer a short epilogue to working life. Many 65-year-olds today can expect to live into their late 80s or early 90s.

NZ Superannuation in its current form was introduced by the Muldoon Government in 1977, with an eligibility age of 60, at a time when life expectancy was around 73 years old. Therefore, the average entitlement to NZ Superannuation was around 13 years. Today, with eligibility at 65 and life expectancy around 83 years, a combination of NZ Superannuation and KiwiSaver is typically required to fund close to two decades of retirement.

For those now in their 50’s, by the time traditional retirement age approaches, life expectancy will have increased further.

Longevity risk is real – both for individuals and the NZ Government when it comes to NZ Superannuation funding.

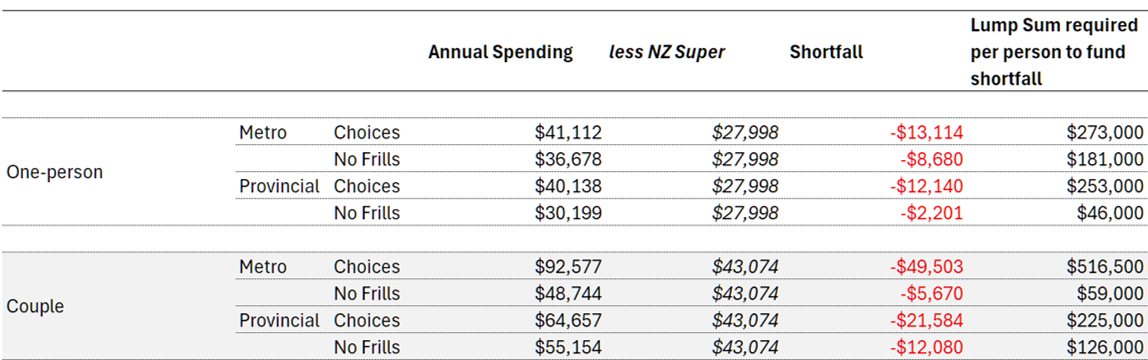

The Massey University Retirement Expenditure Guidelines estimate[2] the amount that New Zealanders need to have saved (in addition to receiving NZ Superannuation) to support different retirement lifestyles. A summary of their data (annualised) is shown below.

While New Zealanders are still heavily reliant on NZ Superannuation, there is a clear requirement to ‘close the gap’ to support a comfortable retirement. These assumptions are, of course, affected by investment returns, inflation and spending levels.

In short – not only does KiwiSaver matter, but the investment strategy we deploy at retirement will need to look very different as we ‘de-cumulate’ investments to support a great retirement.

Enabling retirement: potential investment strategies

Whether spending on your own lifestyle, supporting family members or specific causes, or laying the foundation for significant inter-generational wealth creation is your goal, considering de-cumulation is a critical investment approach.

It’s where a good financial advisor can help. But to help you be an ‘informed customer’ when it comes the ”investment savings” portion of your retirement income, the following may help (note that some approaches can be used in conjunction with others).

| Strategy | Benefits | Risks |

| Fixed Dollar Drawdown withdraw a fixed amount each year | Predictable incomeEasy to budgetSimple to implement | Longevity riskInflation erodes purchasing power |

| Fixed Percentage Withdraw a fixed percentage of starting balance, adjusted for inflation | Simple frameworkHistorically robust within a range of 3.5% to 4.5% | May be too aggressive in low-return environments |

| Dynamic Percentage Withdraw a defined percentage of portfolio each year | Portfolio never fully exhaustedAutomatically reflects market performanceLong-term focus on total returns | Income volatilityOngoing management effort |

| Total Returns approach Withdraw a percentage of the portfolio each year. | A focus on total return investing rather than incomeContinual ‘re-balancing’ of portfolio (eg, income/growth) | Some potential for income variabilityOngoing management effort |

| ‘Bucket’ Strategy Divide portfolio into time ranges and invest accordingly | Manages sequence riskSeparates short-term (income) and long-term (growth) needs | Ongoing management effort |

| Housing Equity Release Reverse mortgage or downsizing | Large cash lump sum | Interest compounding (reverse mortgage)Reduces estate/legacy |

| Planned Spend-Down Capital Exhaustion: design withdrawals so capital is near zero at age 90-95 | Maximises lifetime consumptionEconomically efficient | Risk of outliving assets |

The KiwiSaver debate is centred on both participation and contribution rates – as indeed it should be. The gradual movement towards a “save as you go” superannuation approach will be critical in a world where universal superannuation cannot offer as much as it once could.

For individuals likely to participate in any superannuation transition in New Zealand, keeping a watchful eye on decumulation approaches will become part of our national investment psyche. In the near term, that will require thoughtful withdrawal strategies, understanding the interaction between NZ Super and KiwiSaver, and recognising that retirement is increasingly a multi-decade life stage requiring planning across health, housing, and purpose – not just money.

De-cumulation is not depletion. It is deployment; the deliberate conversion of accumulated capital into a life well lived. Retirement attitudes are changing: it is no longer about being ‘old’ but enabling the opportunities that were simply not an option earlier.

KiwiSaver’s first chapter was about saving. Its second chapter is about spending well to make the most of our lives.

Oliver Mander

[1] https://actuaries.org.nz/content/uploads/2025/09/Retirement-savings-adequacy-RIIG-2025.pdf

[2] https://www.massey.ac.nz/documents/2292/new-zealand-retirement-expenditure-guidelines-2025.pdf

2 Responses

Interesting article. Wish you could convince my husband who, at almost 96, has a managed portfolio which if cashed up today would be worth in excess of $1,000,000, & he also has some money’s with another bank but is terrified of spending any of it, in case he runs out if money before he dies. I am happy to spend often indulgently, but never recklessly. Can’t take it with me wherever I am finally going

That last point feels really relevant – “can’t take it with you wherever I am finally going”. In theory, if you ended with ‘zero’, that is a form of life optimisation! But I do think the behavioural psychology around this is really important. Longevity risk – the fear of running out – is a real thing. And no matter what the probabilities are for the population as a whole, if you’re in that 0.001% that will live for another 15 years, then it hurts. It sounds like the two of you balance each other out nicely!!