NZSA Disclaimer

It has been a tough post-Covid reality check for the New Zealand economy, an underlying theme that is reflected in the performance of many of our consumer-facing listed companies.

Many local companies remembered the difficulty they had in attracting staff in earlier periods during periods of economic benevolence, following cutbacks made during economic gloom. So most have held back from taking drastic action, looking to “survive to 25”. It was only late in the year that things began to turn for the better…with a new mantra of ‘fix in 26’.

Sure enough, underlying economic performance and business sentiment began to turn in late 2025. More recent US and Israeli attacks on Iran, and the resulting energy-price shock, have now interrupted that nascent recovery.

The irony is that many New Zealand investors have performed well over the last five years, despite our local economic performance. That’s been fuelled by increasing investment in international shares and/or funds, with investors receiving the benefit of a boom in AI-related investments and the relatively stronger economic performance of other countries compared to New Zealand.

Currency impacts

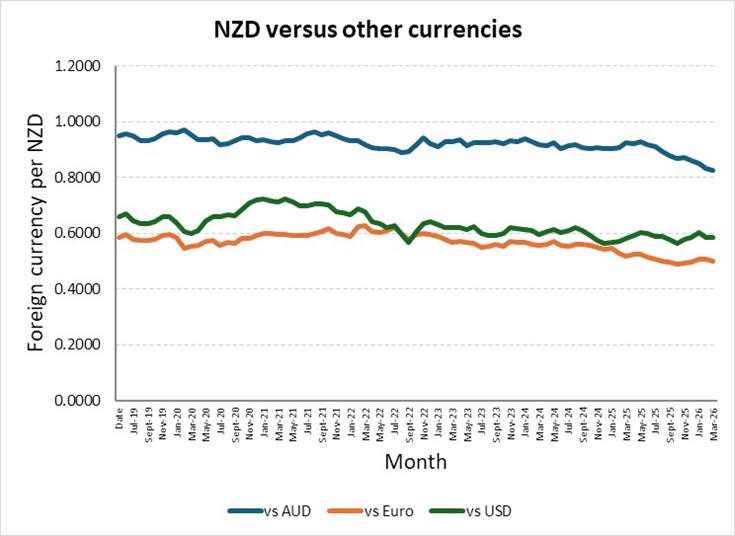

That latter point has provided an additional tailwind for NZ$ investors. A country’s currency can act as a barometer of global expectations, reflecting relative growth prospects, interest-rate settings, commodity exposures and broader risk appetite. In the same way that a share price reflects future expectations of value, the New Zealand Dollar reflects the future value of NZ Inc, relative to other countries.

So as our economy has performed less well than many others, our currency has declined in value against other major benchmarks. As the chart below shows, that trend was already evident before the emergence of the underlying interest rate gap between New Zealand and relevant countries (more on that later).

Our economic recovery may have suffered a setback thanks to the Iranian war; but unlike other New Zealand-specific factors, the impact of the subsequent energy price shock will be felt by all economies.

The value of the NZ$ is not within the control of any single investor. So while Kiwi investors have received a sort of positive ‘double-whammy’ effect from a falling currency, they should be mindful of the potential for that currency effect to unwind over the next 2-3 years should our currency increase in value.

Note that this is not an argument against global diversification. But it is an argument for investors to better understand the options available to reduce currency risk, such as hedging, fund selection and analysing the underlying geographic dispersion of corporate revenues.

Investor Resilience

There is much to impact New Zealand investors beyond currency impacts. The next two to three years are unlikely to be defined by a single market event.

They are more likely to be shaped by the interaction of several forces. As well as currency normalisation that has the potential to unwind previous gains, investors’ returns will also be influenced by global inflation that refuses to disappear quietly, interest rates that may stay higher than investors had hoped, a domestic economy still searching for momentum, reduced consumer demand in international economies, and a global environment in which geopolitical risk is again at the fore of investor sentiment and asset pricing.

That is not a signal for investors to retreat. It does mean they need to be more conscious of the assumptions sitting underneath their portfolios. Investors are now more likely to be facing a world in which the cost of capital remains elevated while household and business demand remains subdued – a sharp change from core assumptions only six months ago.

Inflation and interest rates

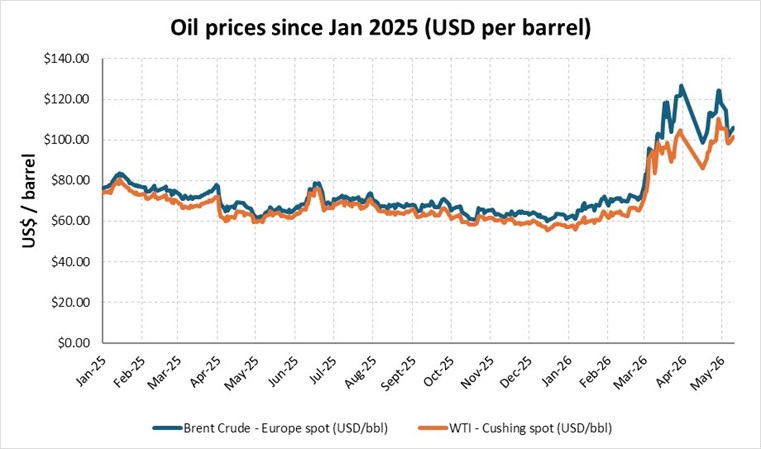

Inflation remains a core risk for investors, particularly when coupled with its impacts on global demand. While governments the world over focus on energy security following the attacks on Iran by the United States and Israel, there is little they are able to do when it comes to oil pricing.

De-carbonisation means that a rising oil price should hold less fear than it did back in the 1970’s, but the impact of oil prices is still felt keenly throughout the global economy. New Zealand has already seen the “first-order” effects, with price increases obvious to anyone filling up at their local service station. More tellingly, however, the Reserve Bank of Australia cited “second-round effects on prices for goods and services more broadly” as a factor in its May 5th decision to increase the Australian Cash Rate Target (equivalent to NZ’s Official Cash Rate) to 4.35%. That means that oil price increases are now finding their way into the broader economic supply chain, with an impact on everything from the price of groceries to clothing.

The increase is meant to dampen consumer spend, to offset inflationary behaviour. Trouble is, for most households and businesses, it is extremely hard to avoid an increase in oil price. For households, that means cutting back discretionary spend elsewhere, reducing demand in the underlying economy. For businesses, that might mean raising prices or reducing staff; again, leading to reduced economic demand.

If inflation remains strong despite underlying increases, thanks to elevated oil prices, the combination of stubborn inflation and reduced demand results in stagflation – a nightmare scenario for businesses and their investors.

In New Zealand, the most recent decision by the Reserve Bank of New Zealand (RBNZ) in early April held the Official Cash Rate (OCR) at 2.25%. While it warned of inflationary impacts, it also noted that it did not want to over-react to oil price inflation and hamper New Zealand’s economic recovery.

Nonetheless, most are forecasting an increase in NZ rates by July (with some forecasting an increase as early as later this month). With NZ inflation forecast to rise to 4.2% in June, we should be under no illusions.

Increasing interest rates are also likely to have an impact on investors. Higher interest rates mean that your money has to work harder to generate a commensurate, risk-adjusted return. In a general sense, that is why share prices fall as interest rates increase, to ensure that the expected yield falls into line with the re-aligned return expectations of investors.

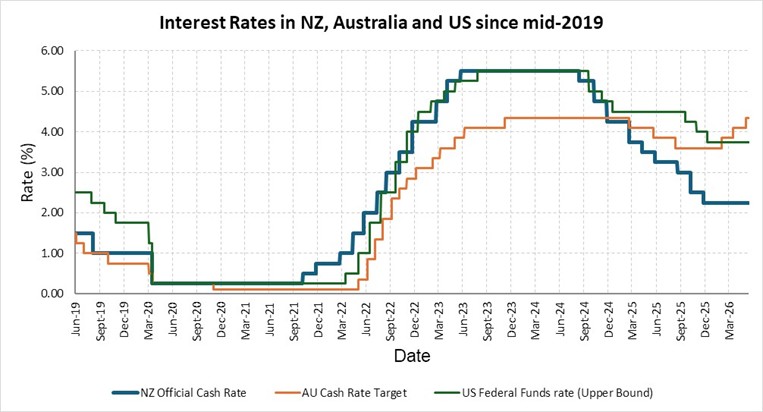

The chart above shows both the stimulatory intention of the interest rates of NZ, Australia and the United States heading into the Covid-19 period, as well as the sharp increases until 2024 as the world grappled with increasing inflation.

It’s notable that Australia did not increase rates as hard or as fast as New Zealand or the US. For New Zealand, this arguably helped to create the conditions for the sluggish economy that reached its nadir during 2024. Since then, the RBNZ has lowered rates (with a positive impact on economic growth), to the point where the cost of money in New Zealand is now markedly lower than those of both our nearest neighbour and the world’s largest economy. One has to go back to 1999 to find the last time the NZ OCR was below that of both these countries for an extended period.

Lower domestic interest rates may provide support for New Zealand asset prices relative to Australia and the US, while income investors could look to Australia as a strong source of fixed income or yield-based returns. But low interest rates do not guarantee higher returns. Investors still need to weigh the benefit of lower discount rates against weak domestic demand, earnings pressure and currency risk.

Economy and geopolitics

In terms of New Zealand, Stats NZ reported 0.2% GDP growth in the December 2025 quarter, following 0.9% growth in September, and Westpac’s May commentary supports a 0.8% March-quarter forecast. Westpac also reflects low and, in some quarters, negative growth for the remainder of the year as a result of the oil price shock.

That tells investors something important: the recovery was present, but fragile, with a likelihood of further deterioration created by geopolitical impacts. A weak domestic economy does not affect all listed companies equally. Exporters, infrastructure operators, banks, retailers, construction-exposed businesses and consumer services companies each experience the cycle differently.

But investors should be careful about assuming that a broad NZ-based earnings recovery will simply follow from lower inflation. Earnings require demand, operating leverage and confidence, not just lower headline interest-rate expectations.

Oil price impacts have the potential for significant second-order effects in New Zealand, as they do in other countries. The conflict has the potential to disrupt global supplies of fertiliser, an essential ingredient that feeds New Zealand’s economic well-being.

Globally, investors have also seen the impacts of key investment themes associated with AI, defence, space exploration and critical minerals. These extend beyond media headlines; all are products of geo-political influences.

For investors, the need to build investment resilience through interpreting the politics has never been higher.

Volatility

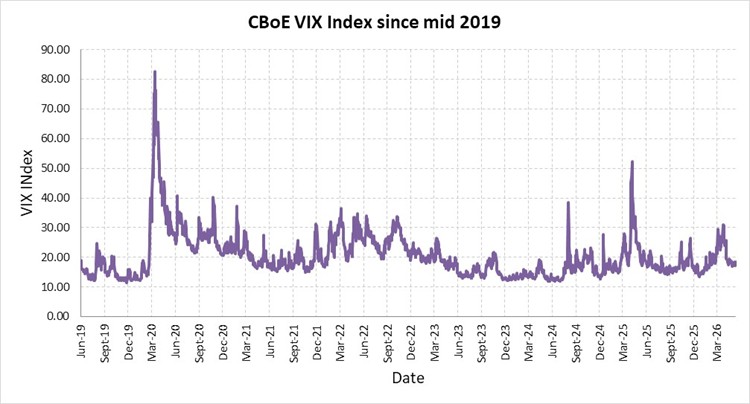

With this context, it is perhaps surprising that investors’ perceptions of risk and volatility have not increased. This is exemplified by the Cboe Volatility Index (VIX), a widely followed ‘fear gauge’ that reflects expected near-term volatility in the S&P 500.

While the ‘spike’ associated with the attacks by the US and Israel on Iran is evident in late March, investors appear to have absorbed the shock more calmly than might have been expected. Even the high point of VIX associated with this event (31.05 achieved on March 27th) is not significantly in excess of “baseline” risk in the immediate post-Covid period of 2021-22, with the investor risk perceptions well below their fears at the time of Trump’s tariff announcements in March 2025.

As a broad observation, that tells us that investors are adopting a cautious view to the underlying risks they face, despite the geopolitics that surround them. At the same time, the level of the index does not indicate complacency, as seen in the immediate period ahead of Covid-19.

The upside

Macro events should always form the backdrop for investor decision-making. Within the shifting sands of economic and geo-political information, there will be opportunity for investors to create their own investment story.

From a New Zealand perspective, we should not take our own investment foundations for granted. Our legislation, legal framework, government institutions (such as the Financial Markets Authority) and various market stakeholders (including auditors, supervisors and capital market participants) are all aimed at supporting confidence in New Zealand’s investment markets. We should not take these institutions for granted. Nor should we take our ability to invest overseas for granted; as investors, we benefit from the free flow of international capital, the ability to accept risks and to organise our own affairs to mitigate them.

With risk comes opportunity.

As investors, we are seeking to maximise our returns given a risk environment. From an investment perspective, that remains the foundation of our society. While recent events have highlighted the importance of resilience in investment portfolios, this should not be news for long-term investors.

For long-term investors, resilience is not a defensive posture. It is the discipline of understanding what risks are being taken, where returns are likely to come from, and which assumptions may no longer hold. The next few years may reward investors who remain diversified, currency-aware and alert to the interaction between inflation, interest rates and geopolitics.

That does not mean retreating from markets. It means investing with eyes open.

Oliver Mander